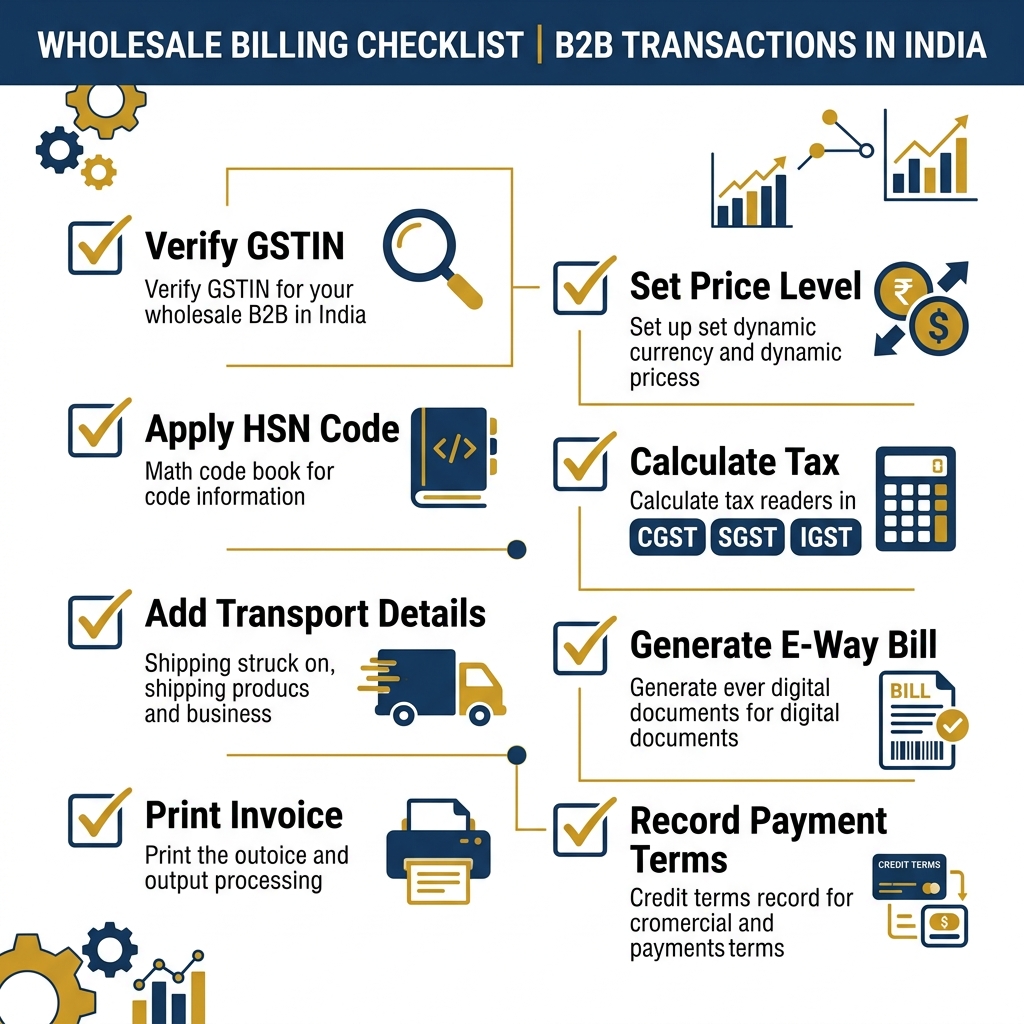

Wholesale Billing Checklist — 14 Things B2B Shops Must Check Before Every Invoice

Rajan runs a plywood wholesale business in Nagpur. Good guy, decent turnover — about ₹1.8 crore a year. Last September, he shipped ₹3.5 lakh worth of marine plywood to a furniture manufacturer in Pune. The tempo left at 6 AM. By 11 AM, Rajan got a phone call from his driver — the goods were detained at a checkpost near Ahmednagar.

No e-way bill.

Rajan's billing clerk had generated the invoice but forgot to create the e-way bill because the consignment was split across two invoices — one for ₹2.1 lakh and one for ₹1.4 lakh. He assumed each was under ₹50,000 threshold. They weren't. The combined shipment crossed the limit, and the GST officer knew exactly what to look for.

Penalty? ₹18,000 plus the goods were stuck for two days. Rajan's customer was furious. The furniture order was delayed, and the customer shifted half his business to another supplier.

All because of a missing checkbox.

I've been helping wholesale businesses sort out their billing for years now, and I'll tell you — most losses don't happen because of bad products or high prices. They happen because of sloppy paperwork. A wrong GSTIN here, a missing LR number there, and suddenly you're bleeding money you didn't even know you were losing.

So here's my wholesale billing checklist. Print it out. Stick it next to your billing computer. Make your staff read it every morning if you have to.

For a deeper dive, read our e-way bill threshold rules.

1. Verify the GSTIN — Every Single Time

I can't stress this enough. "But sir, he's our regular customer, we know his GSTIN" — I hear this constantly. And then what happens? The customer changes his business structure, gets a new GSTIN, and nobody tells you. You keep billing on the old number for three months.

Your customer can't claim ITC on those invoices. Now he's angry. Now he's asking you for credit notes. Now your CA is pulling his hair because the GSTR-2A reconciliation is a disaster.

Here's what to do: Go to services.gst.gov.in, click "Search Taxpayer", and punch in the GSTIN. Check three things — trade name, legal name, and registration status. If it says "Cancelled" or "Suspended", stop. Do not bill. Call the customer.

In Tally Prime, there's actually a built-in GSTIN validation feature. Go to Gateway → Alter → Stock Group or Ledger → and enable "Validate GSTIN." It'll flag mismatches. Busy Accounting has a similar check under Administration → Configuration → GST Configuration.

One more thing — if a customer gives you a GSTIN from a different state than his delivery address, ask questions. That's a red flag for fake ITC claims, and you don't want to be dragged into someone else's mess.

2. Get the E-Way Bill Right

The ₹50,000 threshold applies to the consignment, not individual invoices. If you're loading multiple invoices in the same vehicle going to the same place, the combined value matters. Rajan learned this the hard way.

Generate the e-way bill before the goods leave your godown. Not after. Not "I'll do it in 10 minutes." Before.

Part-A is the invoice details. Part-B is the vehicle number and transporter details. Both must be filled. I've seen wholesalers fill Part-A and leave Part-B blank because "the transporter will fill it." The transporter won't. He has 50 other shipments to worry about.

And update the vehicle number if it changes mid-route. If goods are transhipped to another vehicle, you need to update Part-B on the portal. Yes, it's annoying. Yes, it's necessary.

3. Price Level Management

This is where wholesale billing gets messy fast. You have different prices for different customers. Your Hyderabad distributor gets 18% off MRP. Your Nagpur retailer gets 12%. The big-volume buyer in Indore gets 22% but only on orders above ₹2 lakh.

If your billing clerk doesn't have a proper price list system, he's going to make mistakes. And nobody catches these mistakes until the end of the month when a customer calls saying "you charged me ₹40 extra per sheet on 200 sheets."

That's ₹8,000 gone.

In Tally, set up Price Levels under Inventory Info → Price Levels. Create separate levels — "Distributor", "Retailer", "Bulk Buyer" — and assign them to each party ledger. When you create a sales voucher, Tally automatically picks the right price.

In Busy, go to Administration → Masters → Price List. Same concept. You can even set date-wise price levels for seasonal pricing.

Point is — don't rely on your clerk's memory. Memory fails. Software doesn't.

4. Transport Terms: To Pay vs Paid vs To Be Billed

This creates more arguments than you'd expect. "To Pay" means the receiver pays the freight. "Paid" means you've already paid. "To Be Billed" means you'll be billed later by the transporter.

Mention this clearly on the invoice. If the customer expects To Pay and you've marked it as Paid, he'll refuse to reimburse you. And you'll eat the freight cost — which on a Nagpur to Pune load can easily be ₹3,500 to ₹5,000.

Also mention the transporter's name and GSTIN. Under GST rules, if freight is charged separately and the transporter is registered, you need to mention this for proper tax treatment.

5. LR Number on Every Invoice

The Lorry Receipt number is your proof that goods were handed over to the transporter. Without it, you have no proof of dispatch. If the customer claims "goods not received", you're stuck.

I know a steel trader in Raipur who lost a ₹1.7 lakh dispute because he couldn't produce the LR. He had dispatched the goods, the transporter confirmed it verbally, but there was no LR number on the invoice or in his records. The customer denied receiving the material and the trader had no legal ground to stand on.

Get the LR from the transporter. Note it on the invoice — either at the bottom or in the transport details section. In Tally, you can add this in the Dispatch Details section of the Sales Voucher.

6. HSN Codes — Don't Wing It

I see this constantly. Billing clerks typing random HSN codes or leaving them blank. "Sir, I'll fix it later." Later never comes.

Wrong HSN code means wrong tax rate classification. Wrong tax rate means mismatch in GSTR-1. Mismatch means notice.

For businesses above ₹5 crore turnover, 6-digit HSN codes are mandatory on every invoice. Between ₹1.5 crore and ₹5 crore, you need at least 4 digits. Under ₹1.5 crore, technically optional — but I'd still recommend it.

Keep a master HSN list for your product categories. In Busy, you can assign HSN codes directly to stock items under Masters → Item Master. Once set, they auto-populate on every invoice.

7. Invoice Numbering — Sequential, No Gaps

Your invoice numbers must be sequential. No gaps, no duplicates, no "oh we cancelled that invoice so we skipped the number."

GST law is clear — invoice series should be consecutive. If the department finds gaps during an audit, they'll assume you issued invoices for unaccounted sales. Good luck explaining that.

Both Tally and Busy handle auto-numbering well. Set it up once — prefix, starting number, and financial year suffix — and don't override it manually. Ever.

8. Delivery Address vs Billing Address

B2B bills sometimes have three addresses — your address, the customer's registered address, and the actual delivery location (a warehouse, a project site, a different branch).

Get these right. If the delivery address is in a different state from the billing address, you might need to charge IGST instead of CGST+SGST. Your e-way bill also needs the correct delivery pin code for distance calculation.

I've seen invoices where the billing address says "Mumbai" but the goods went to Thane. Technically a different district. These small things create problems during assessments.

9. Credit Note Discipline

Returns, rate differences, damaged goods, quantity shortfalls — all of these need credit notes. Not verbal adjustments, not "I'll deduct it from the next bill", not WhatsApp messages saying "adjust ₹4,500."

A credit note under GST has specific requirements:

- Reference to the original invoice number and date

- Reason for the credit note

- Tax amount being adjusted

- Must be reported in your GSTR-1 by November 30 of the following financial year

If you delay credit notes past the deadline, you lose the ability to reduce your output tax liability. That's real money gone to the government that you can't get back.

Set a rule: credit notes must be raised within 7 days of the return or complaint. Not 7 weeks. Days.

10. Payment Terms — Write Them Down

30 days? 45 days? COD? Part advance, part credit?

Put it on the invoice. I don't care if you've been trading with this customer for 15 years and "everyone knows the terms." Put it in writing.

When it's on the invoice, you have legal backing for recovery. When it's verbal, you have an argument. There's a ₹4.2 lakh difference between the two — that's the average disputed amount I've seen in wholesale billing fights.

11. Quantity Cross-Check Before Dispatch

Your billing clerk types 500 pieces. The packer loads 480. Customer receives 480, invoice says 500. Now what?

Have a simple gate pass system. Before the goods leave, someone — not the packer, someone else — counts and signs. The gate pass should match the invoice quantity. Any difference gets flagged immediately.

In Tally, you can create a Delivery Note voucher that's separate from the Sales Invoice. The delivery note captures actual dispatched quantity. Compare the two at the end of the day.

12. Discount Structure Documentation

Trade discount, cash discount, volume discount, scheme discount — how many types of discounts are you giving? And are all of them reflected on the invoice?

GST requires that discounts given at the time of sale should be mentioned on the invoice for proper tax calculation. If you give a discount of ₹10 per piece but don't show it on the invoice, you're paying GST on the higher amount. You're literally paying extra tax for no reason.

Post-sale discounts (like year-end incentives) need to be handled through credit notes. Don't just adjust them informally.

13. Round-Off Consistency

Small thing, but it bites. Some shops round off to the nearest rupee. Some round off to the nearest ₹10. Some don't round off at all. Be consistent.

If your round-off method doesn't match what your software calculates, you'll have tiny differences that accumulate. At the end of the year, your books might show ₹3,000 to ₹5,000 in unreconciled round-off differences. Not a huge number, but try explaining that to an auditor.

14. Backup Your Invoices

Look, this isn't a billing rule per se. But I've seen two businesses lose everything — one to a hard disk crash, one to ransomware — because they didn't back up. Their entire invoice history, party ledgers, stock records — gone.

Tally has an auto-backup feature. Enable it. Set it to daily. Keep a copy on a separate drive or use the cloud sync option.

Busy allows scheduled backups to external drives and cloud storage. Set it up on day one and forget about it.

By the way, also keep a physical copy of high-value invoices — anything above ₹1 lakh. PDF print, save it in a folder. Takes 30 seconds and can save you lakhs.

B2B Wholesale Billing Key Checklist Summary

The Real Cost of Sloppy Billing

Let me do some rough math. Say your wholesale business does ₹1.5 crore annually. If even 2% of your invoices have errors — wrong price, missing credit note, GSTIN mismatch — you're looking at roughly ₹3 lakh in disputed amounts, delayed payments, lost ITC, and penalties.

₹3 lakh. That could be your entire profit margin on ₹30 lakh worth of sales.

A checklist costs you nothing. A billing error costs you everything.

Print this list. Put it where your billing person can see it. Run through it for a week until it becomes habit. After that, it becomes automatic — like checking your mirrors before reversing.

Frequently Asked Questions

What is the minimum invoice value for generating an e-way bill?

You need an e-way bill for any consignment value exceeding ₹50,000. This includes the taxable value plus GST. Some states like Karnataka and Kerala have lowered this threshold for intra-state movement, so always check your state's specific rules. Don't try to split invoices to stay under the limit — that's a well-known trick and officers look for it.

How do I verify a customer's GSTIN before billing?

Go to the GST portal — services.gst.gov.in — click "Search Taxpayer", and enter the GSTIN. Check the trade name, legal name, and registration status. If the status says anything other than "Active", don't issue a tax invoice. In Tally Prime, enable auto-verification under the GST settings of the party ledger. Busy has a similar feature under GST Configuration.

What happens if I bill on the wrong GSTIN?

Your customer loses the ability to claim Input Tax Credit on that invoice. You'll need to issue a credit note against the wrong invoice and then create a fresh invoice with the correct GSTIN. This also creates mismatches during GSTR-2A/2B reconciliation, which can trigger a notice from the department. I've seen cases where the customer simply refuses to pay until the corrected invoice is issued — so now you also have a cash flow problem.

Should wholesale bills always include HSN codes?

For businesses with turnover above ₹5 crore, 6-digit HSN codes are mandatory. Between ₹1.5 crore and ₹5 crore, 4-digit codes are required. Below ₹1.5 crore, they're technically not mandatory but I always recommend adding them. Clean HSN mapping prevents tax rate mismatches and makes your GSTR-1 filing smoother. Also, if your customer is above the threshold, he'll want proper HSN codes on your invoice for his records.

What is the difference between To Pay and Paid in transport billing?

To Pay means the receiver (your customer) pays the freight charges upon delivery. Paid means you, the sender, have already paid the transporter before dispatch. There's also "To Be Billed" which means the transporter will bill the sender later. This must be clearly mentioned on the invoice and the lorry receipt to avoid disputes about who owes the freight. Get this wrong and you'll argue for weeks over ₹4,000.

How long do I have to issue a credit note under GST?

A credit note must be declared in your GST return by the 30th of November following the end of the financial year in which the original invoice was issued, or the date of filing the annual return — whichever comes first. If you sell goods in January 2026, you have until November 30, 2026 to declare the credit note. After that deadline, you cannot reduce your output tax liability. Don't sit on credit notes — process them within a week.